Profits tax in Hong Kong – Complete Guide

As favored by business owners for its low tax rates and simple taxation structure, Hong Kong is booming as a global hub and investment center not only in Asia, but also around the world. Hong Kong has been ranked 4th in the world as the easiest place to set up a business.

Other than the advantages of easy business formation structure, companies can also enjoy tax incentives and allowances for further reducing the tax liabilities for their business, whether they are abroad or in Hong Kong. As a result, this helps to lessen the tax burden on your company and create opportunities for greater economic freedom when doing business.

What’s more, if you are expecting to conduct your business operation outside of Hong Kong or none of your business activity arises from or is derived in Hong Kong, then you may be able to claim for the tax exemption status.

If you are a serious entrepreneur who is willing to start a Hong Kong company, then you should gather all the important information about profits tax in Hong Kong. If you don’t know the tax system in place, and how filing profits tax in Hong Kong works, then this is a good place to start.

This article will let you know about the profits tax involved when an individual, a partnership or a body corporate (i.e., company) works while carrying on business in Hong Kong.

Let’s dive deeper-

Profits Tax in Hong Kong

Hong Kong follows a territorial system for corporate tax arising in or derived from the city. In short, it means that it is the geographical ”source of the income.” In Hong Kong, there are 3 general types of taxes: Salaries Tax, Profits Tax, and Property Tax.

Profits tax is an income tax that is chargeable to businesses carried on in Hong Kong. As per the Inland Revenue Ordinance(IRO), it is levied on the “assessable profits” of legal persons whether it is a sole proprietorship, corporations, partnerships, trustees or persons carrying on any trade, profession or business in Hong Kong.

Profits Tax Filing Requirements & Deadlines

You may wonder what the requirements and deadlines for the filling of profits tax in Hong Kong are. As stated earlier, profits taxes are payable by every company carrying on a profession, trade, or business in Hong Kong on profits arises or derived from it. And if a Hong Kong company conducts business outside the city, it may be eligible to claim offshore tax exemption.

The profits derived from a foreign source, which is often known as ”offshore profits”, are thus generally beyond the territorial scope of Hong Kong’s taxation system, including those derived by locally incorporated companies.

From incorporation, all registered businesses are generally tracked by the tax authorities of the IRD (Inland Revenue Department). And after checking all the details, they issued a tax return for the first anticipated “year of assessment”.

In case a company conducts business during a particular financial year, but does not receive a PTR (Profits tax return), it should notify the IRD and file its accounts on an annual basis.

Hong Kong’s Tax Year

In order to fulfill the requirements of filing profits tax in Hong Kong, you need to know about Hong Kong’s tax year. The tax year is in a fiscal year starting in April, not the typical calendar year from January to December.

Ultimately, the ending date of the fiscal year for Hong Kong is March 31st and the PTR also follow the same model. As a result, 2020 (2019/20) PTR will be for the period from April 1st, 2019 until March 31st, 2020.

While setting up a business in Hong Kong, it is up to each business to select their financial year. Which financial year end is best for you normally depends on your business cycle or requirements of tax recording that suits you best.

Therefore, if your company’s year-end is on December 31st, 2019, then these financial figures will be used to fill in the 2020 PTR for the company.

The PTR filing can also be extended for older companies with an established financial year end for certain year-end dates, but this needs to be applied for each year for the filing extension.

The dates for the extension of filing are as below:

Financial Year ended as at 31st of March

- Tax Filing Date – 15th of November

- Documents Ready for Audit – Not later than 1st of September

Financial Year ended as at 31st of December

- Tax Filing Date – 15th of August

- Documents Ready for Audit – Not later than 1st of June

Financial Year ended as at Other dates than a) or b) e.g. 30th of June

- Tax Filing Date – 30th April

- Documents Ready for Audit – Not later than mid of February

1st Filing Tax Request

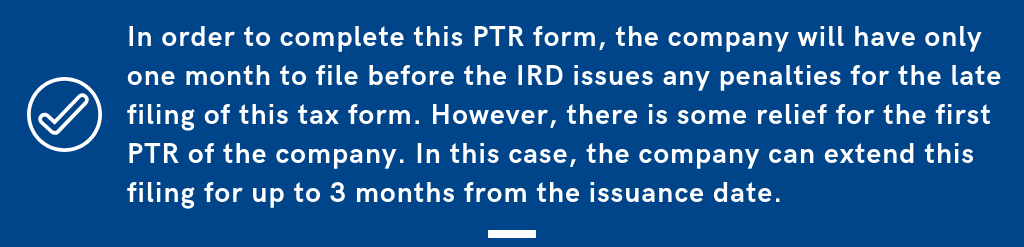

So, when you are required to file a request for your very first profits tax of the company? Approximately after the 18 month mark from the incorporation date of your company, the first PTR will be issued. For instance, if a company was incorporated on 01 January 2018, it will receive its first PTR from the government around June 2019.

And if your business has commenced either in Hong Kong or abroad during this period of time, then you need to prepare all the financial accounts for it. Regardless of whether the business operations have been conducted outside of Hong Kong, you still need to report it’s accounts and any profits earned in the annual reports, to claim the profits tax exemption.

Furthermore, you are also required to complete the PTR and submit it together with the supporting documents within three months from the date of issuance. This normally will include the Audit Report of the financial statements, which can only be prepared by a Hong Kong Certified Public Accountant. A professional CPA can help you prepare the audited financial statements and completing the PTR filing for the company.

What kind of Source of Income Subject to Profits Tax?

In Hong Kong, the following types of sources are subjected to pay profits tax-

- Entities trading within Hong Kong; and

- Income arising from such trade; and

- Profits arise in or are derived from Hong Kong

Hence, while paying for profits tax, it doesn’t matter whether you are resident or non-resident of Hong Kong. A non-resident can earn a profit during their business operating in Hong Kong chargeable to profits tax, and a Hong Kong resident can derive profits from abroad without being charged tax in Hong Kong.

You may be thinking whether your profit is derived from Hong Kong or not. This typically depends on the questions of fact, ie. the hard facts and evidence that show the location of your trade or business operations. But still, there are some guidelines on the principles applied in some cases which have been considered by the courts in Hong Kong and other common law jurisdictions.

In the regards of tax assessment of “source of income,” this factor has been generally explained as the geographical location of an entity’s operation which substantially raises its income.

Here are some factors in determining the location of profits of a business

1. Location of a sales contract being negotiated and executed

The first question that may come to mind for new business owners is, ‘Where was the physical place where a sales contract was negotiated and signed?” The location of this may play a large factor in determining the location of business of the company.

This can further be explained by looking at two scenarios-

When income is deemed as Hong Kong source income for profits tax purpose:

When the seller in Hong Kong negotiates the sales or purchases in a contract to a buyer in Hong Kong, or someone who is living outside the territory, through the means of electronic communication or telecommunication so that the negotiation did not require travel outside the territory. It can be e-mail, messaging services, teleconference, facsimile or telephone.

When income is NOT deemed as Hong Kong source income for profits tax purpose:

In this kind of situation, the income is not deemed as Hong Kong sourced income for profits tax when a contract was signed and negotiated outside the territory of Hong Kong, with sufficient documentary evidence. And also when the goods were not sourced from within the territory.

2. Shares & Securities

When you derive income from securities purchased and sold in the Hong Kong stock exchange, your income is deemed as Hong Kong sourced income for profits tax purposes. Regardless of the jurisdiction of incorporation and the nationality, the entity is subject to profits tax on such an activity.

3. The Establishment of an Office in Hong Kong

Normally the establishment of an office in Hong Kong would classify the business operations as occurring in Hong Kong, as the decisions of the management for the business occur within the city. The extent of the role of the office in Hong Kong would determine if the business would be subject to profits tax in Hong Kong.

What are the Profits Tax Rates & How can you claim for Profits Tax Exemption?

By now you may have a better idea about which kind of income would be deemed as Hong Kong sourced income. And more importantly, on which kind of income you may claim as a tax exemption. As the profits tax is normally applied to all businesses, some exceptions occur for non-resident entertainers and sportsmen.

The details of the profits tax rates in Hong Kong are as follows:

- Unincorporated Businesses (i.e. Sole-Proprietorship and Partnership): first HK$ 2 million chargeable income is 7.5%; the remaining is 15%

- Non-Resident Entertainers and Sportsmen: 15% ~ 16.5% flat rate

- Corporations (i.e. Company): first HK$ 2 million chargeable income is 8.25%; the remaining is 16.5%

How can you claim for Profits Tax Exemption?

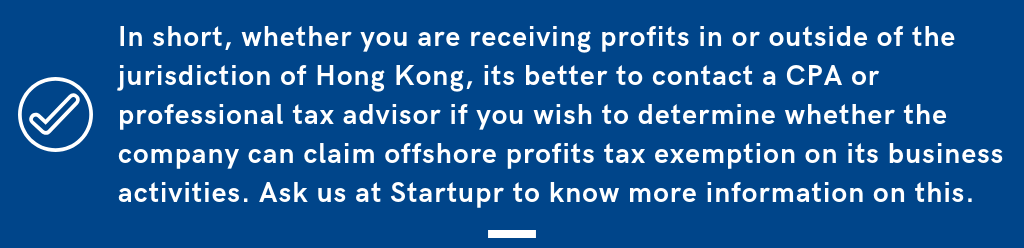

Another question that comes up is how can you claim profits tax exemption for your company? This query has been asked by many entrepreneurs while setting up their business.

When your HK business is operating entirely from outside the jurisdiction of Hong Kong, then your business entity may qualify for Profits Tax Exemption. This kind of operation is granted by the tax officers of HK after review of the company’s operations and financial details.

Hong Kong works on the territorial system for corporate tax derived or arisen from Hong Kong. Therefore, if your profit is derived outside of Hong Kong, then these profits may not be subject to corporate taxation in the city, regardless of whether the funds are remitted through Hong Kong or other territories.

As a result, if the company receives funds to a bank account in Hong Kong, but still conducts trade outside of Hong Kong, they may not be subject to corporate profits tax. On the other hand, if the funds of the company is received to an offshore bank account, but the company is trading within Hong Kong, it may be subject to corporate profits tax.

Which documents are required to submit to the IRD in order to claim for tax exemption?

The company must file the annual set of returns with the following documents in order to claim for this:

- The completed Profits Tax Return (PTR) as issued by the IRD

- A tax computation showing the amount of assessable profits(or adjusted loss)

- A certified copy of your statement of Balance sheet, Auditor’s report, and the Statement of Profit and Loss in respect of the financial year

If you want to prepare these documents properly and enjoy the benefits of profits tax exemption, then these documents should be prepared by a Hong Kong Certified Public Accountant, who would review the company accounts and generates an audit report and tax computation for the company.

How can Startupr Help you?

If you have made up your mind to set up a company in Hong Kong, then Startupr can help you every step of the way. We will help you in providing all the important and updated information in accounting or taxation which you may come across while operating the business.

Otherwise if you already have a company, and would like more information about the accounting, taxation or filing profits tax in Hong Kong, we can assist you as well. We can act as your tax representative and take care of filing the PTR and communicating with the Hong Kong IRD.