Hong Kong Tax Return

The simplified tax regulations and low-tax regime make Hong Kong a booming city and an investment center not only in Asia but around the world. Many business owners have started establishing their ventures in Hong Kong to enjoy the business-friendly environment and tax incentives and allowances.

When operating a Hong Kong business, you should be aware of the taxation system and how it works for business entities. If you haven’t established your business in Hong Kong yet, but are curious to know the different rules and regulations of Hong Kong taxation, this article will help you know the ins and outs of the tax regime and Hong Kong tax return.

Taxation in Hong Kong

Hong Kong is renowned among entrepreneurs for its low taxation regime. The corporate taxes are levied at just 8.25% on the first HKD 2 million in profits, and 16.5% thereafter. There are no sales taxes, VAT taxes, withholding tax on dividends and interest, capital gains tax, tax on dividends, and estate tax. This is why businesses and individuals in Hong Kong enjoy one of the most tax-friendly systems in the world.

Even though Hong Kong follows a simple and straightforward taxation regulations, below are the most defining aspects of Hong Kong taxation you should be aware of:

- Hong Kong corporate tax (profits tax)

- Salary tax in Hong Kong

Let’s read about these taxes and the rules and regulations that business entities need to follow to operate a business in Hong Kong smoothly.

Hong Kong corporate tax (profits tax)

The corporate tax on Hong Kong companies is charged at an 8.25% rate on the accessible profit earned for profits under HKD 2 million, and a 16.5% tax rate thereafter. The possible taxation after the chargeable profits may be further reduced by the allowances and tax deductions for businesses.

Corporate income tax base period

The base period for paying corporate tax in Hong Kong runs from April 1st until March 31st. The city follows this fiscal year and asks business owners to file corporate and salary taxes as per their business earnings. If you have set up a new business in 2020, the year of assessment for 2020/21 will be the fiscal year starting from April 1st, 2020, and ending on March 31st, 2021.

In Hong Kong, corporations reserve the right to select their own financial year as per their business operations, however most companies choose either December 31st or March 31st because of tax return filing extensions for these year ends. For more information regarding corporate tax rate in Hong Kong, click here!

Salary tax in Hong Kong

The next important tax that you should be aware of is salary tax in Hong Kong. Hong Kong also has low taxation regulations for personal income tax or salary tax. It is levied at a standard 15%, and follows a progressive tax rate system with some of the world’s lowest rates. However, people also enjoy allowances on non-taxable income and taxes paid in arrears.

The total income above the salary allowances and deductions will be taxed as per HK taxation rates. So, if you earn less than the allotted allowance less deductions, you may end up paying very little or no tax in Hong Kong!

Personal income is generally used to determine the net chargeable taxation over the fiscal year.

Assessable income is calculated as:

Total income – non-assessable income – permitted deductions – personal allowances = net taxable income

Considering the allowances in the year of 2019/20 (April 1st, 2019 to March 31st, 2020), all personal income over the basic allowance of HKD 132,000 would be directed to the progressive salary tax rates. If you are earning less than this income level, you would not be liable to pay any HK salary tax.

As soon as the individual’s tax payable is calculated, this is further reduced by a tax reduction. So for the year 2019/20, the tax reduction is 100% of the tax payable up to HKD 20,000.

Who all needs to pay personal income tax?

The personal income tax is levied on all individuals whose income source is from an office, pension, or employment (subject to salaries tax) in Hong Kong. According to the territorial principle of Hong Kong, the income will be taxable when it has a primary source in Hong Kong. This same theory applies to self-employed individuals who are operating a business, but instead of salaries tax they pay profits tax.

Here are some income categories under personal taxation in Hong Kong

- Salary, employment wages and director’s remunerations

- Bonuses, commission income and paid leave from the company

- Company stock awards or stock options from the company

- Employment termination payments and retirement benefits such as MPF

- Rental compensation from property offered by the employer

- Pensions

Tax Return in Hong Kong

Taxes are levied on the income sourced from the trade, business, or any profession, partnership business, or a non-resident person to profits tax in your name. If you are qualified under these conditions, you need to complete the profits tax return and any required supplementary forms. Moreover, individuals must also file the PTR to the Inland Revenue Department (IRD) by the due date.

Profits tax return for corporations (PTR)

The profits tax return for companies will be issued by the Inland Revenue Department in April every year. The company will have one month to file the accounts after the issued PTR from the IRD, however they may also extend their PTR filings after their first financial year-end (2nd year onwards).

If you have recently set up a company, you may receive the first tax return 18 months after incorporation. Within the three months from the issued date, the completed PTR needs to submit to the IRD. If the company somehow is late for the PTR submission, the IRD reserves the right to impose stricter penalties for non-compliance for PTR filings.

If you are looking for assistance in filing your company’s PTR, Startupr can help! We offer assistance and consultation for taxation matters and other information in regards to corporate taxation, personal taxation, and company formation. Feel free to get in touch with us for further details.

Parts of the profits tax return

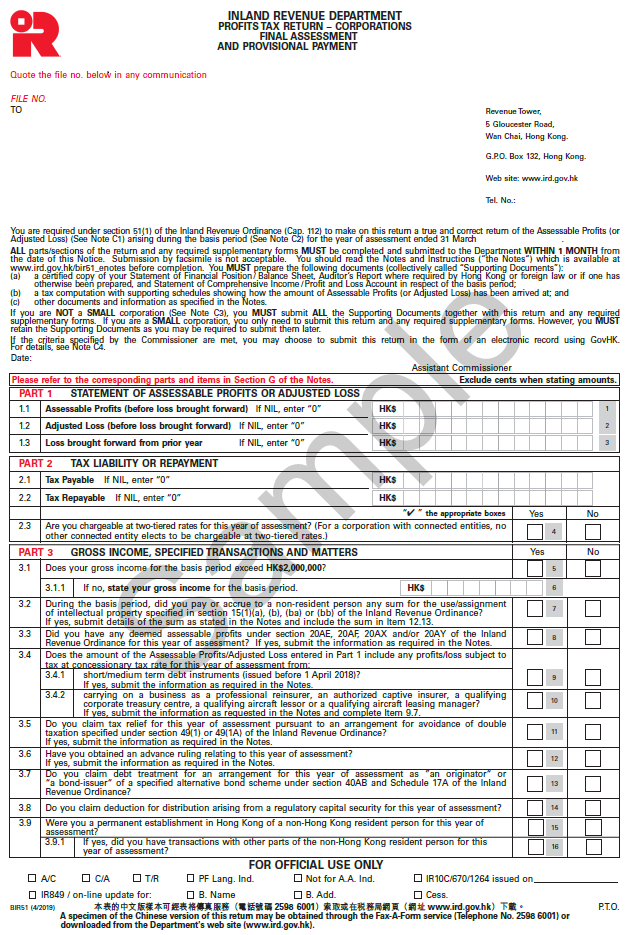

Now let’s dive into the different sections of the Profits Tax Return for incorporated companies, and what information you would need to fill this out.

- Part 1 (STATEMENT OF ASSESSABLE PROFITS OR ADJUSTED LOSS) – In this section, state the total amount of assessable profits (taxable profits) or adjusted loss (tax deductible loss) and any loss brought forward from prior years. You can find these numbers from the company’s tax computation.

- Part 2 (TAX LIABILITY OR REPAYMENT) – This section is used after calculating the total amount of tax payable or tax repayable from the government for the company, being taxed at the two-tiered rates in Hong Kong.

- Part 3 (GROSS INCOME, SPECIFIED TRANSACTIONS AND MATTERS) – State here the gross income (all types of income) during the year, and answers to specific tax matters such as payment to non-residents for IP, relief from double taxation, Advanced rulings and Permanent establishments in Hong Kong.

- Part 4 (DETAILS OF THE CORPORATION) – Here state the important details of the corporation like the contact number, principal business activity, HK SICC (Standard Industrial Classification Code) and product/service.

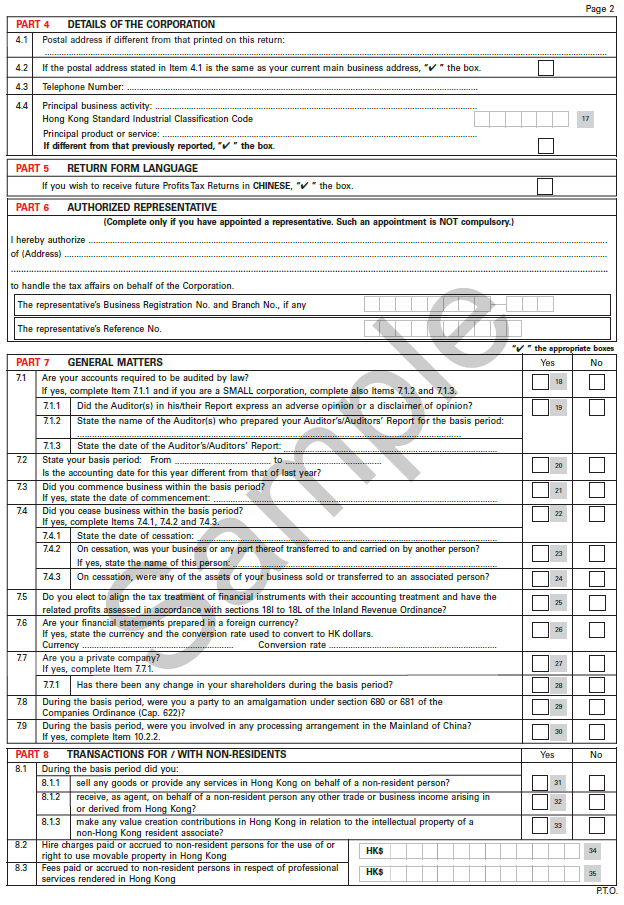

- Part 6 (AUTHORIZED REPRESENTATIVE) – In this section state the particulars of the authorized tax representative of the company.

- Part 7 ( GENERAL MATTERS) – The general matters section is for the basic information of the company accounts, such as the auditor’s information, accounting period, commencement or cessation of business, foreign currency and others.

- Part 8 (TRANSACTIONS FOR / WITH NON-RESIDENTS) – If you had any transactions for or with non-Hong Kong residents, you should put the details here, such as selling good or services, as well as fees paid during the year.

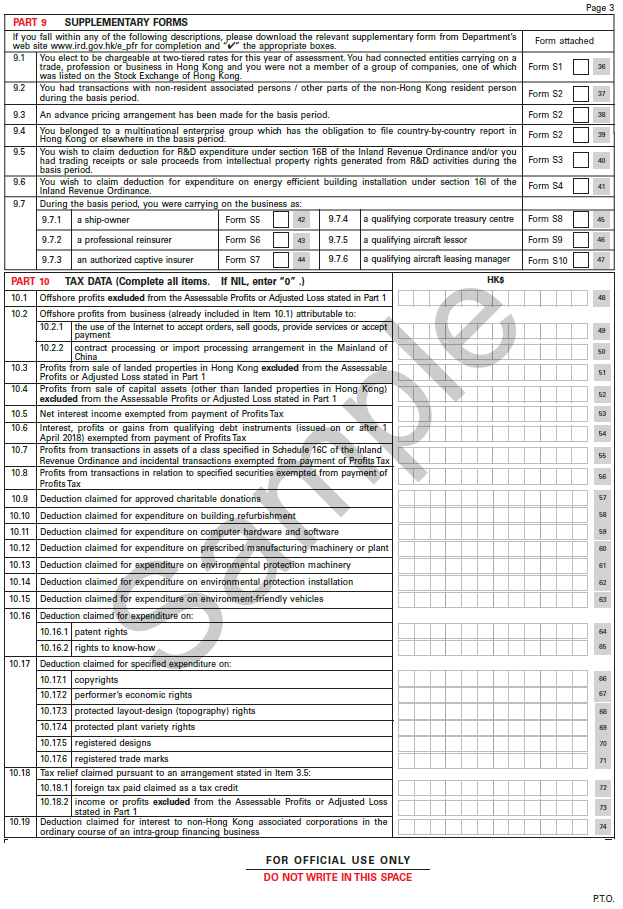

- Part 9 (SUPPLEMENTARY FORMS) – This is a relatively new section and includes adding additional separate supplementary forms for connected entities, advanced pricing arrangements, MNEs with country-by-country reporting, carrying on business in certain business sectors, and others.

- Part 10 (TAX DATA) – This section pertains to tax deductions and exclusion of income from assessable profits, such as offshore profits. If your company has tax deductions or offshore income to declare, this is where you would include the data.

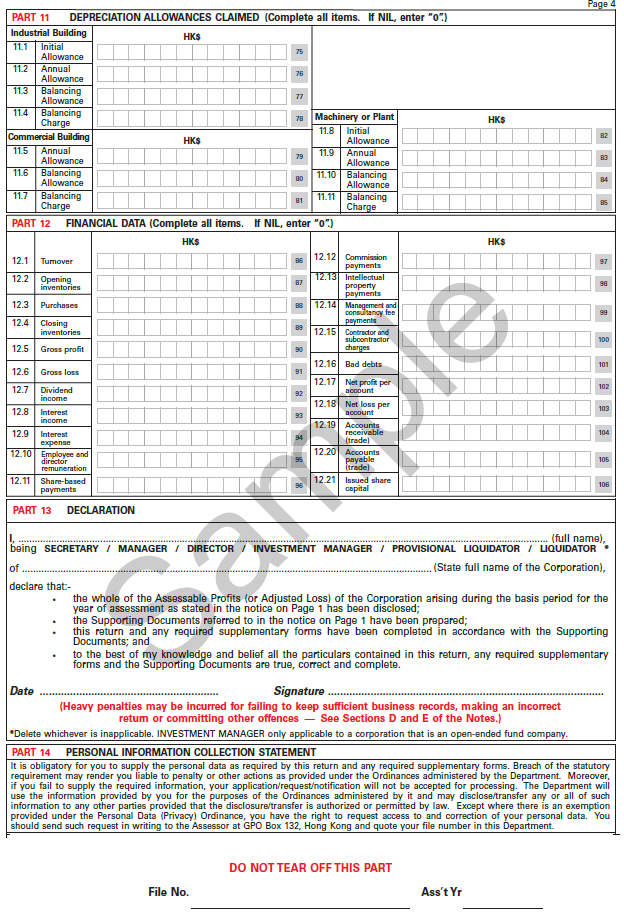

- Part 11 (DEPRECIATION ALLOWANCES CLAIMED) – If your company had any depreciation allowances on fixed assets (Industrial Buildings, Commercial Buildings, Machinery or Plant), then the amounts (either the Initial Allowance, Annual Allowance, or both) would be included here.

- Part 12 (FINANCIAL DATA) – The summary of the company’s financial data (Revenue, Cost of sales, expenses, Account receivables and payables and issued capital) would be entered here. Be sure to fill in the specific expense accounts if this applies to your company.

- Part 13 (DECLARATION) – This part is for the declaration of the PTR filer, their role, and the company’s name.

Here is a sample of what the PTR looks like:

The downloadable version can be found at IRD website

When to file?

Usually the profits tax return and the supplementary forms need to be filed within one month of the issued date. The submission date is specified on page 1 of the profits tax return. However for the first PTR received for a company, they would have up to 3 months to file this form. Additionally, companies can apply for a general extension for their 2nd PTR and onwards.

If you want to file the tax return through electronic ways, the department may grant an extension. The extension may be given 2 weeks after the normal due date, subject to the small partnership businesses, and small corporations will file the profits tax return via the internet.

Documents and information to be prepared and submitted

Corporates need to file the profits tax return with the following documents:

- The issued and completed PTR with the IRD.

- A certified copy of your statement of the Balance sheet, Auditor’s report, and the Statement of Profit and Loss in respect of the basis period

- A tax computation stating the amount of assessable profits (or adjusted loss).

Generally these documents are prepared by a Certified Public Accountant (CPA). They will be responsible for reviewing the company accounts and generating an audit report and tax computation. They will act as the tax representative and be responsible for completing the PTR and tax calculations for its assessable profits.

Audited financial statements and Hong Kong CPA

Under the Hong Kong Companies Ordinance, all the companies incorporated in HK need to have an annual audited financial statement processed or reviewed by a HK CPA. In Hong Kong, it is the auditor’s responsibility to review all the company’s accounts and obtain sufficient appropriate audit documentation for each company. They will not only keep an eye on your company accounts, but they will also look for the appropriate records if the IRD requests for further documentation. This may be especially true if the company is applying for offshore tax exemption.

Personal or Individual Tax Return

Personal or individual taxes are assessed on the income earned or derived within Hong Kong from taxpayers. If you are employed in a Hong Kong company, your complete salary would be chargeable to the year’s salary tax. On the other hand if the income is earned from outside Hong Kong, in general you would be exempted from salary tax under that year of assessment, except if you work as civil servants or crew members of an airline.

The next situation where you can claim for salary tax exemption is when you are employed in Hong Kong for services less than 60 days. Here, the nature of your trip would be assessed by the IRD based on the documentation provided.

Filing of personal tax return

Hong Kong individuals must file an annual tax return to the IRD. This city follows the fiscal year ending on March 31st, so the taxpayer would normally receive the individual tax return form by May 1st. They then would need to complete and submit the form within one month from the issued date.

Let’s suppose if you haven’t earned a single penny or didn’t reach the limit of taxation, you still need to file your Hong Kong tax return. But here you would need to declare your income as zero, and the IRD would assess the completed form and check whether any other tax needs to be paid and send a demand note to the taxpayers. If any taxpayer feels that there are some miscalculations of the tax payable, they may send an objection letter to the IRD within 30 days.

Sole-proprietors are also required to file their operations during the tax year on the individual tax return (Part 5 of personal HK tax return).

If you have any questions regarding Hong Kong salary tax or personal tax forms, Startupr can help. We offer assistance in taxation matters and other information in regards to corporate taxation, personal taxation, and company formation. Feel free to get in touch with us for further details.

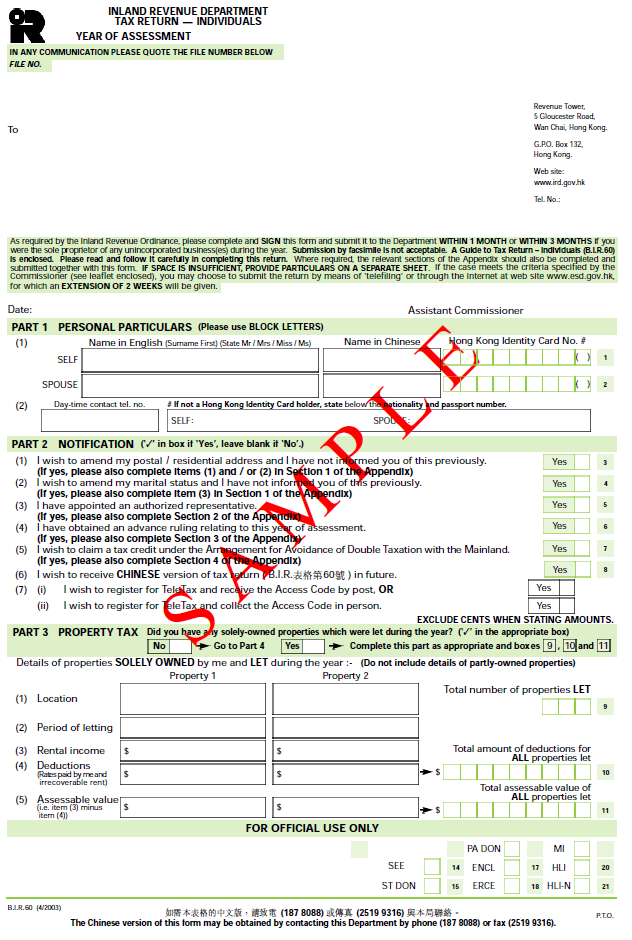

Part of the Personal Tax return

Next let’s take a look at the different sections of the Personal Tax Return for individuals and what information you would need to fill this out.

- Part 1 (PERSONAL PARTICULARS) – Put in your personal information like name, spouse’s name, contact number and Hong Kong ID or Passport number.

- Part 2 (NOTIFICATION) – This section is for specific notifications you would like to inform the IRD about, such as residential address changes, marital status, tax representation, advanced rulings and double taxation with Mainland China.

- Part 3 (PROPERTY TAX) – This part is for individuals with solely owned property rented out during the year, and the particular information about these premises.

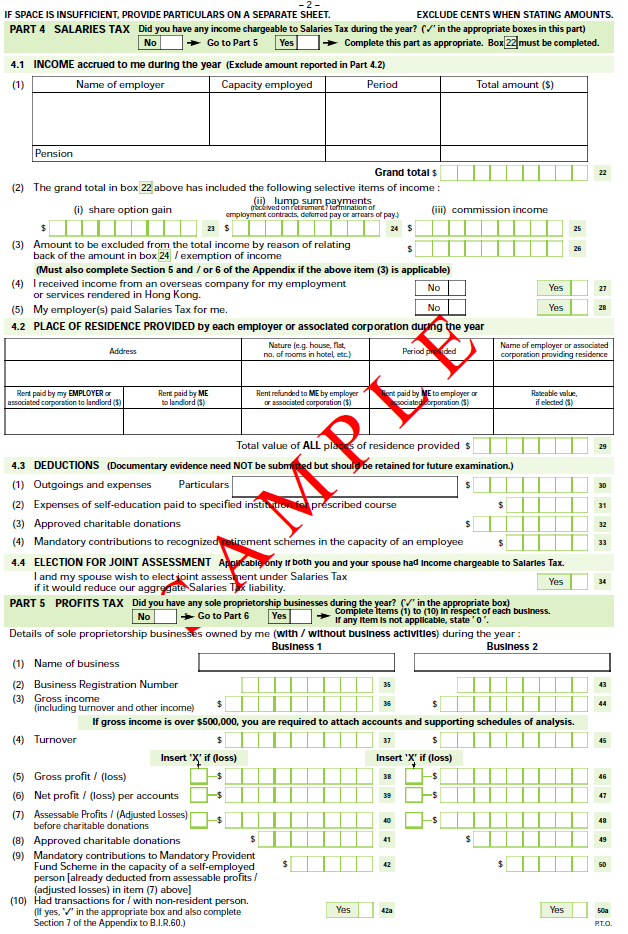

- Part 4 (SALARIES TAX) – This is where you enter in your total income earned during the year as salaries. It includes your income (part 4.1), which should match your received Employers Return (IR56B, or like W-2 form in the US), any housing benefits you received (part 4.2) and any taxable deductions (part 4.3).

- Part 5 (PROFITS TAX) – This section is for individuals who have a sole-proprietorship and declare their total business activities and financial information here.

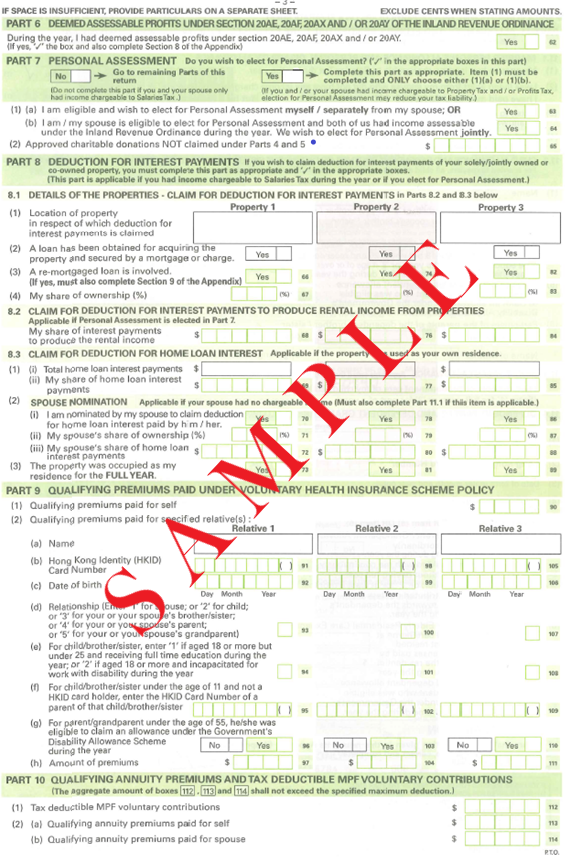

- Part 7 (PERSONAL ASSESSMENT) – This is where you declare if you want your taxable income to be as a personal assessment or joint assessment.

- Part 8 (DEDUCTION FOR INTEREST PAYMENTS) – This section is for declaring deductions on interest payments for solely/jointly owned property.

- Part 9 (QUALIFYING PREMIUMS PAID UNDER VOLUNTARY HEALTH INSURANCE POLICY) – This part is for premiums paid for certain health insurance policies. Be sure to check out the maximum allowed deductions and the acceptable health insurance policies from the IRD website.

- Part 10 (QUALIFYING ANNUITY PREMIUMS AND TAX DEDUCTIBLE MPF VOLUNTARY CONTRIBUTIONS) – Here enter in a certain types of MPF voluntary contributions that are qualifying annuity premiums (different from regular employee related MPF contributions declared in part 4.3).

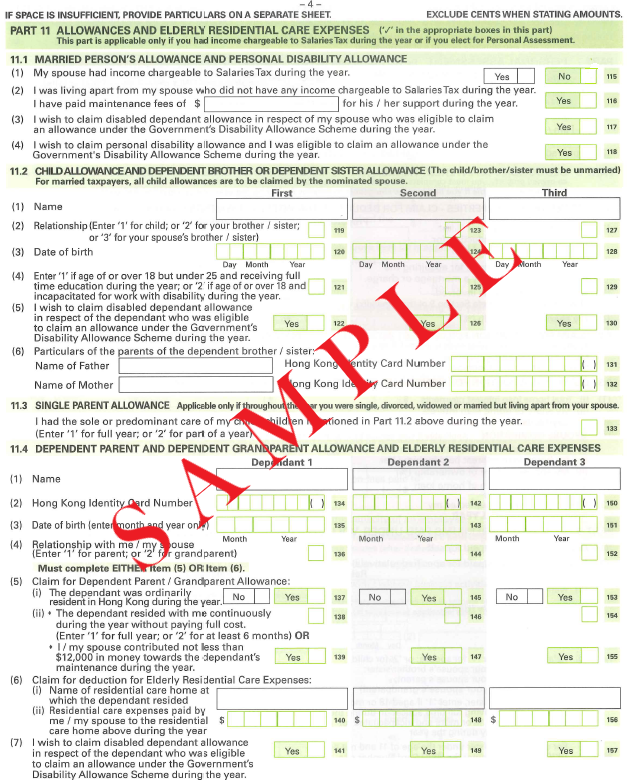

- Part 11 (ALLOWANCES AND ELDERLY RESIDENTIAL CARE EXPENSES) – Fill out this part for married persons allowances and declared personal disability allowances, child allowance and dependents (brother sister), single parents, and dependent parent/grandparent and elderly residential care expenses.

Here is a sample of what the Hong Kong Individual Tax Turn looks like:

The downloadable version can be found at IRD Website

When to file?

Usually the IRD issues the annual tax return to taxpayers as per the fiscal year of assessment. So most taxpayers receive their tax return form on 1st May of every year. It needs to be filed and completed within one month from the issuance date. For more information about the filing and completion of the form, feel free to contact Startupr.

Documents and information to be prepared (Employers return)

By now, you may have a better idea about the profits tax return and salary tax return that needs to be filed with the IRD. However, some people still wonder what an Employer’s return(ER) is.

For most individuals, their employers’ salary payments will constitute the majority of the total income generated over the year. Like any other jurisdiction in the world, HK businesses are also required to file the total annual salary and retirement payments (MPF) for every employee to the IRD. This specific income will be recorded in the Employer’s return form for every HK company.

As soon as the Employer has filed the ER to the IRD, they will send one copy to their employees, which the figures would be used to file their own personal tax form. The IRD will refer to these figures when reviewing each individual’s total tax payable.

How to calculate taxes?

Personal income is generally used to determine the net chargeable taxation over the fiscal year. The income over the allowances and less deductions would be needed to figure out or calculate the taxable income using the progressive rates.

Below is the table of professive tax rates for each Year of Assessment:

| Year of Assessment | Profit Earned | Tax Rate |

| 2014/15 to 2016/17 | 0 to 40,000 HKD 40,001 to 80,000 HKD 80,001 to 120,000 HKD Above 120,001 HKD | Rate is 2% Rate is 7% Rate is 12% Rate is 17% |

| 2017/18 | 0 to 45,000 HKD 45,001 to 90,000 HKD 90,001 to 135,000 HKD Above 135,001 HKD | Rate is 2% Rate is 7% Rate is 12% Rate is 17% |

| 2018/19 onwards | 0 to 50,000 HKD 50,001 to 100,000 HKD 100,001 to 150,000 HKD 150,001 to 200,000 HKD Above 200,001 HKD | Rate is 2% Rate is 6% Rate is 10% Rate is 14% Rate is 17% |

Let’s say, you are eligible for the basic allowance in the year 2019/20 (April 1st 2019 to March 31st 2020), so all your income over the basic allowance of HKD 132,000 would be directed to the progressive rates of the salary tax.

Therefore, if you earned HKD 400,000 during the year (Approximately USD 51,200), you would have income of HKD 268,000 over the basic allowance, subject to tax. On the first HKD 50,000 you would be charged 2% (HKD 1,000), on the second HKD 50,000 charged 6% (HKD 3,000), on the third HKD 50,000 charged 10% (HKD 5,000), on the fourth HKD 50,000 charged 14% (HKD 7,000) and on the remaining HKD 68,000 charged 17% (HKD 11,560). This is a total of HKD 27,560 in taxes.

Now with a tax reduction of 100% for taxes up to HKD 20,000 in the year 2019/20, that means you would only owe HKD 7,560 in taxes, meaning around an effective tax rate of 1.89% ($7,560/$400,000) for the year. This example shows how the low tax regime of Hong Kong can favor not only individuals but also for Hong Kong businesses operating in the city and worldwide.

You may also refer to the IRD online tax calculator to better estimate your taxes in Hong Kong.

How Startupr can help you?

This article is all about the Hong Kong tax returns that you should be aware of. If you are not sure about the procedure of submitting the forms, and how much tax you would need to pay, Startupr can help.

As taxes are a staple for every business entity and individual, if you find difficulty complying with your tax obligations or need more information, feel free to contact us. We work closely with CPA professionals and have helped thousands of Hong Kong companies file their accounts and tax returns over the years. Contact us today!